Restraining the size of state government requires restricting its access to revenue. Governments tend to consume whatever revenue is in front of them. The best way to keep state government from growing faster than a state economy is to constrain access to revenue. Many states are effectively controlling the cost of government operations. Most states and the federal government are struggling to restrict growth of social programs.

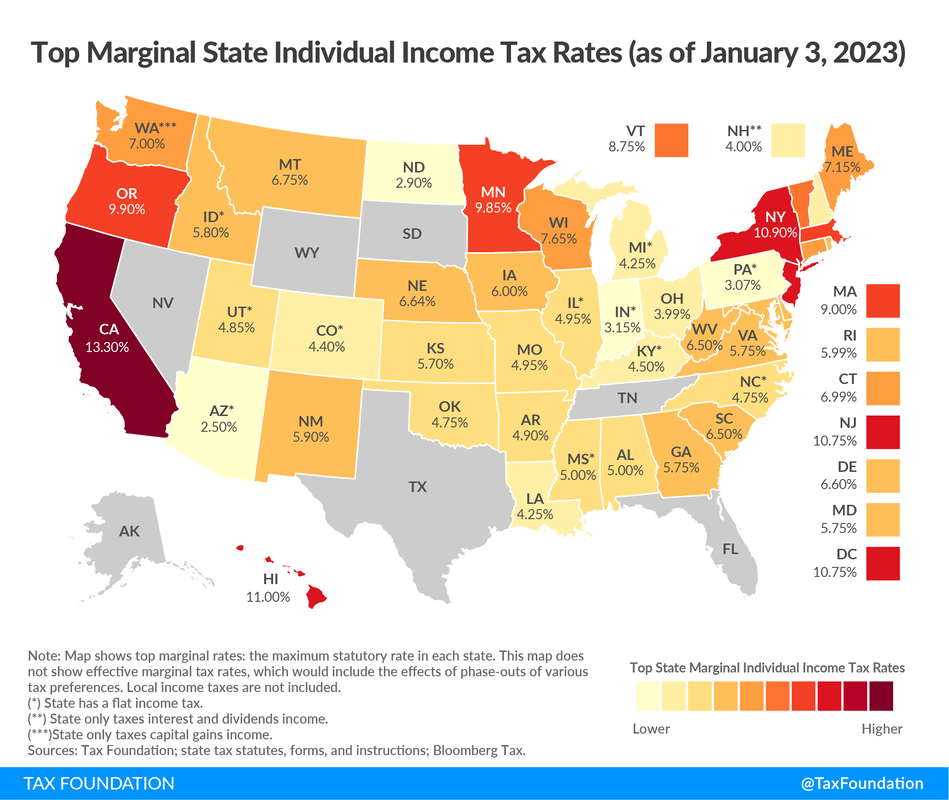

The Utah House of Representatives voted to eliminate the sales tax on food subject to voters choosing to removing the constitutional earmark that historically reserved income tax funds for spending on education. I was one of a few who opposed the bill. Following are the reasons why: Eliminating the Sales Tax on Food is Less Effective than Reducing Income Taxes While I am for reducing taxes wherever we can, there is a large surplus in the income tax fund and better policy would have been to reduce income taxes further than the legislature has proposed this session. The current income tax reduction proposal will reduce the rate from 4.85% to 4.65%. This reduction is estimated to be $380 million in ongoing tax relief. Applying the $200mm sales tax on food reduction to income tax relief would get Utah very close to a 4.5% income tax rate. We are going to have to find ways to keep reducing income tax when Nevada and Wyoming are at 0%, Arizona is at 2.5% and Colorado is at 4.4%. Eliminating sales tax on food also impacts local cities and counties who rely on sales tax as a part of their budget. Utah Can Continue to Successfully Balance Its Budget One of the most common arguments for removing the constitutional earmark is the need for budget flexibility. This refrain is not new. In 2019 we were told that if we didn't increase sales tax revenue then the state would not be able to balance its budget. We were also told that in time of recession the sales tax was too volatile. Looking back at the 2020 recession, both assertions were incorrect. Sales tax proved more stable, income tax proved to be more volatile, and Utah successfully balanced its budget. Utah is Considered the Best Managed State Our state has lead on nearly every metric of state fiscal responsibility. On removing the earmark, we are not leading. We are following many other states who have not managed their state as effectively as Utah has. Our success is due to good leadership, but it is also do to balanced budget requirements and restrictions on the general fund. Social Services Spending Growth is Unsustainable Medicaid, Medicare, Social Security, and related programs in the United States Federal Budget are the largest budget line item and are growing faster than the economy. Because there are no constraints to contain expenditures and because we all genuinely want to help children, the disabled, and the elderly, our deficits are over $1 trillion annually and growing. In Utah, social services is the largest line item at approximately $8.5 billion and one of the fastest growing. Historically, our social services spending has been constrained by the resources available in the general fund. Utah weakened the constraint when we amended the constitution to include spending on children and the disabled, but this final step removes any remaining constraints the earmark might have had on social services spending. Summary It is very difficult to constrain spending in government. The most effective constraints on spending are those that limit resources. The constitutional earmark limited the growth of the largest, fastest growing portion of government. If the citizens vote to approve the constitutional amendment, it will be up to the legislature and the citizens to do the hard work the earmark has done for us over many decades contributing to Utah's status as the best managed state. Semantics: "the meaning of a word, phrase, sentence, or text" (Oxford Languages, 2022 09 07).

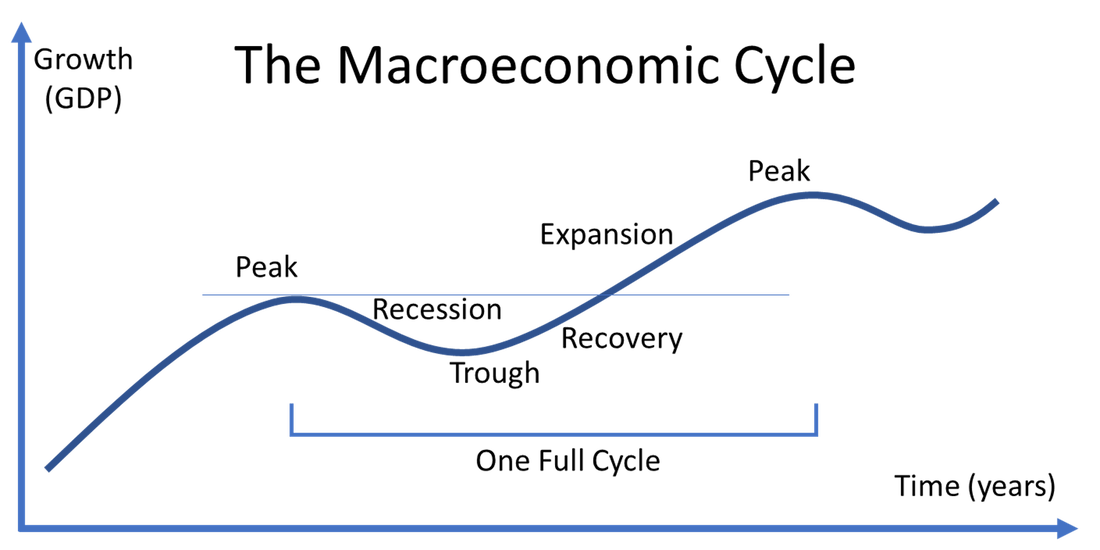

Over long periods of time, the meaning of words change. The context for their use may change, the way they are used may change, and their frequency may change. "Square" in the 1950s was used differently and more frequently that it is today. "Lit" is not just lighting, or literature, it is cool or legitimate. These examples are the result of youth repurposing a word in a way adults hadn't considered. Today we are seeing a change in the meaning of the word for political purposes. Inflation is a simple word, if we have inflation then prices are rising. In the spring of 2021, the United States government made an effort to explain rising prices as something else. Rising prices weren't inflation, they were "transitory" or temporary. The efforts to redefine the word because it wasn't popular to recognize inflation when it surfaced resulted in policy choices that entrenched inflation. Inflation will end when one or more of the following occurs: the supply of money is reduced, demand for goods and services falls, and/or productive capacity increases. It is difficult to fight inflation with higher interest rates when policy choices increase disposable income (forgiving student loan debt) and increase supply costs (eliminating fossil fuels). As long as fiscal policy (government spending and taxation) and regulation is increasing demand and constraining supply, the Federal Reserve's monetary policy efforts to reduce inflation through higher interest rates are sterilized. We will see inflation rates fall, but price levels are likely to remain high. Recession is another word fallen prey to semantics. Recession has historically been defined by two consecutive quarters of falling real GDP. The first quarter of 2022 saw real GDP fall by 1.6%. This means the output of goods and services in the United States fell by 1.6% compared with the same quarter in 2021, on an annualized basis. The second quarter saw real GDP fall by .6% compared with the second quarter of 2021. Traditionally, this would be a recession. Because employment and wages increased during this time, prices were rising (inflation), and calling a recession was not expedient, the government has been unwilling to identify the recession of 2022 as a recession. There are other words the government is trying to change. Man, woman, male, female, racist, and capitalist are all facing transitory meanings. When you look at the words around these words you can see the meaning changing. Such as, "I identify as a man". In the past, it wasn't the choice of the individual to identify or not identify. You were or you were not. A racist was someone who labeled people by race, class, or some other category and deemed them inferior. A racist is now someone who does not accept the labels applied to them by others. A capitalist was someone who took care of themselves and created opportunity for others by responding to the forces of supply and demand. Now a capitalist is someone who takes advantage of others using market power and influence. Who will defend the words? If we choose to change their meaning, what words do we use to say what we used to mean? The solution to economic prosperity is straightforward. Fiscal responsibility, sound money, and stable regulatory policy. The solution to our identity is not to rewrite history, whitewash it, or redefine it, it is to learn from it and be better today because of it.  United States of America is still the most powerful economic influence in the world. If we choose to "drill baby drill", over the long run we will simultaneously erode Russia's financial ability to wage war on Ukraine and others by driving global energy prices down and slow inflation. This would begin the liberation of Eastern Europe from Russian influence through economic policy.

As natural gas supplies increase, we can re-route liquefied natural gas exports from China to Europe. As we engage Canada, open the Keystone XL pipeline, and enlist Mexico, we can reduce revenues to Russia and limit China's access to low cost energy resources. We can use our enormous energy resources to support our allies and weaken governments led by autocrats claiming a democratically elected mandate. As an economic policy, capitalism beat communism and ended the cold war in the 1980s and we can do it again. Russia and China both acknowledged the failure of their centrally planned economic systems and moved to a form of capitalism to retain their political power. As a system of governance, communism has no better track record. Supposedly free elections are overshadowed by fear, censorship, and oppression. A truly free people would not chose the ruthlessness that governs the two Asian nations. On equality and opportunity, Russia and China have made the political class in the two countries wealthy in a way that would make the robber barons of the early 1900's blush. While they pay lip service to their citizens, they coerce them into systematic oppression and trap them in long term poverty. The wealth creation of western economies and the spontaneous innovation of free people will always outmatch centrally planned economies and their political class. This is why they can't wean themselves off a form of capitalism. We should untether the us economy and demonstrate unequivocally that there is no economic system that can match it. We should not move forward with a 1960’s dual mandate of guns and butter. To leverage the economic strength of this country, we need to demonstrate the kind of fiscal policy that will firmly establish the United States as the global standard for fiscal stability, budget accountability, and credit worthiness. A United States Government that is not dependent on its allies or aggressors for financial support would demonstrate the impact for good that free markets, free governments, and free people can make in the 21st century. On defense, we should be the most respected nation in the world both because of our capability and our restraint. If we can’t lead from the White House, we should lead from the respective states. Let states set in motion a wave of capitalism and freedom that will demonstrate the influence for good that God given rights protected by Constitutional governance, including life, liberty, property, and the pursuit of happiness can have on the lives of our people. Real estate markets in 2021 showed historic gains as prices soared on low inventory.

Looking ahead, these six drivers will impact housing markets in 2022. Population Shifts The trend toward the south and the intermountain west accelerated as employers became more flexible with work-from-home options and higher-ed has expanded online learning. Migration that favored large urban centers with high concentrations of employment and education is now leaning toward recreation, tourism, and open space. Materials and Labor Shortage Lumber prices shocked the real estate world in the spring of 2021. Now, steel prices are setting records and materials are in a rolling shortage. On the employment side, 23% of employees are expected to change jobs in 2022. Key people and key materials remain in short supply and working out supply logistics will take time. Capital Expansion Rising stock markets and rising real estate values coupled with direct capital infusion from federal government stimulus means there is more money than ever circulating in the economy. This expansion of capital is searching for investments. Unfortunately, every time capital is placed in the stock market or the real estate market, a seller has capital returned that needs to be re-invested. This is driving prices up and returns down. Interest Rates Both short-term and long-term interest rates will be determined by Fed policy. Expectations are that Fed stimulus will be withdrawn and short-term interest rate increases are imminent. If these actions slow the economy or impact employment gains in California, New York, or Illinois, expect the Fed to pump the brakes and resume more accommodative policies. Inflation Along the I-15 corridor, more demand, materials and labor shortages, more capital to invest, and low interest rates mean higher real estate prices in 2022. While the CPI hit 7% for December, housing measured only a 4% increase while home prices rose over 20% in most markets in 2021. Inflation is higher than reported. Affordability One of the most difficult real estate challenges is affordability. It is compounded by rising home prices and limited supply. Affordability can be improved by rising wages, falling home prices, or lowering interest rates. In 2022, wages, home values, and materials are all expected to rise. It is a challenging time for housing affordability. Conclusion While we won’t solve the affordability problem in 2022, we do know that over a lifetime, owning beats renting consistently. Long-term housing stability and closing the wealth gap in the United States both point to home ownership. For more information please visit https://erabrokers.com/research/ The last twelve months have seen sentiment in residential housing markets change dramatically. The result is one of the most dynamic and challenging housing markets in memory. Following is a brief overview of market conditions over the past twelve months and a look at what to expect in the second half of 2021. Summer 2020 The summer of 2020 ended the first wave of COVID-19 cases and with it came a sense that the pandemic might be easing. As individuals and families considered their housing circumstances, their employment, their school opportunities and their personal constraints, they looked to move. Early in the summer, supply was plentiful and buyer demand—although increasing—was not driving multiple offer scenarios. Rental eviction moratoriums were being enforced and mortgage forbearance was widely available. With interest rates at record lows, moving to a home that provided safety from the virus and accommodated work and school circumstances started the wave of home buying. Fall 2020 An accelerating wave of COVID-19 cases in the fall increased buyer activity as people sought refuge from the pandemic and policies that restricted movement. With relocations increasing, existing housing inventory began to fall. Buyers entered the market faster than sellers offered homes for sale setting up multiple offer. Builders, who just a few months ago were concerned about oversupply, found they had no inventory to sell. Many builders had released commitments in the spring and were now looking for lots, land, labor, and materials to ramp up their homebuilding operations. Interest rates remained near record lows and rents began to rise. Spring 2021 As COVID-19 cases fell from winter peaks and vaccinations rates rose, we experienced one of the most challenging markets for buyers ever recorded. What began as multiple offers turned into dozens of offers in many cases. The supply of available homes was measured in days, not months, and many builders moved to sell finished units only. Supply chain challenges and labor shortages became acute and seemingly everyone was following record high lumber prices. Builders renegotiated contracts and missed delivery deadlines. Sellers asked for tens and hundreds of thousands of dollars over ask and required buyers to waive due diligence and financing contingencies. Prospective sellers were unable to move because they couldn’t find a new home to move into, deepening the shortage and accelerating the price appreciation. Summer 2021 Moving into the summer, lumber prices began to stabilize and then fall. Existing home inventories increased, although inventories remain lower than during the summer of 2020. Price levels are much higher, although price increases seem to be stabilizing. Some sellers are asking too much for their homes, taking themselves out of the market. Appropriately priced homes are still seeing multiple offers, although far from the frenzy of the spring. The COVID-19 Delta variant began a third wave of rising case numbers since the pandemic began. Second Half 2021 Looking ahead to the fall and winter, we believe the same drivers are moving the market that we identified at the beginning of 2021. Home as a safe place is the number one priority for most home owners and renters. Individuals and families are still looking for a place to educate their children, work, and play while remaining safe from COVID-19. The increased flexibility of work arrangements are accelerating relocations. The recent increase in cases has some employers extending their work-from-home accommodations, which in turn has employees moving to the place where they want to live while keeping their job. Low interest rates are softening the impact of higher prices as monthly payments remain manageable for many individuals and families. While inventories are higher than the past spring, overall inventory remains far below historical levels and far from oversupply. What’s Ahead Inventory levels should increase, bringing them closer in line to historical levels. Supply constraints will continue to disrupt builders, but not at the same level as the past spring. Rental demand will remain high and rental units will remain under supplied, causing rents to continue to rise in most markets. Price levels are at risk if interest rates rise, remote employees are called back to the office, or builders get ahead of market demand. Given the current conditions, we expect prices to rise in the second half of 2021, although more slowly than in the first half of the year. For more information visit https://erabrokers.com/research/ One year ago, in March 2020, State and Local Governments put the United States into a recession in response to the global COVID-19 Pandemic. From the outset, it was apparent this recession would be unlike the past recession, or any other in our memory (see my post from March 19, 2020). It set in motion structural changes in our economy that will last decades. V, U, W, K Recovery As soon as the recession was declared, economists tried to describe the shape of the recovery. The first forecasts were for a sharp recession and a proportionally sharp recovery, a “V”. As COVID surged in a second wave during the summer, the concern became a long recovery and a long bottom, or a “U” shaped recovery. The improving economics in the fall lead to fears of a fall recovery and a winter retrenchment, followed by a more sustained recovery in the spring, or a “W” recovery. It is clear, that the COVID-19 recession will be something different, a “K”. A “K” shaped recovery is an economic cycle with a sharp downturn, followed by sectors that boom and others that bust. This bifurcated recovery is painful as some languish under frustratingly dismal conditions while others watch their economic outlook brighten. Value stocks languished in bear territory following the spring correction while Tech was responsible for the S&P reaching an all-time high at the end of the year. Big box retail saw tremendous pressure on sales while industrial distribution centers experienced record demand. Apartments in the densest urban cores are saw lease rates fall more than 20% while suburban and rural housing saw record high price levels. Tourism destinations such as New York City, Hawaii, and Las Vegas were hit very hard while destinations near national parks in states that did not close performed well. Restaurants with large dining rooms struggled to remain open while drive-thrus saw record sales. Non-essential employees who could not work from home became unemployed while essential and remote enabled roles remained employed and may have thrived. Unfortunately, K-12 education, one of the most resilient sectors in any recession, has not been spared the bifurcated outcomes. While budgets were hit with technology and curriculum modifications, the bigger impact was students who could continue to attend in person versus those who could not. Parents and students without means were disproportionately impacted by closed schools. With children at home, parents may have had to choose between essential jobs and their child’s education. Education is a means to opportunity, and many were set back by policies that kept children home without necessary technology, supervision, and support. Structural Population Shift Since the Industrial Revolution, people have migrated to cities for education and employment. While the country was historically dominated by small farms and agricultural jobs, the industrial revolution resulted in technology and productivity gains that transformed farming and created opportunity in nearly every other industry. The result was generations of better jobs and upward mobility concentrated in urban centers. These urban centers have housed the nation’s largest employers and attracted talent from across the country. In many instances, employers are there because they were looking for a deep pool of human capital and the infrastructure to support their growth. Over decades, state and local governments set policy with the knowledge that employees would be required to work where their employers were headquartered. While technology was enabling remote work and remote education for a few prior to the pandemic, COVID-19 may have broken this relationship between employer and geography by allowing millions of jobs to move remote nearly overnight. Live, work, play is a movement that has been upended by COVID-19 and the structural shifts in its wake. It used to be that we lived where we worked. Now, many may have the opportunity to live anywhere. If they have that choice, will they choose to live where they play? Will they relocate to be near family? Will they choose to live in expensive urban centers? We have already seen that many are willing to relocate if their employer will allow them. This is a potential reversal of a migration trend that could favor most communities in the country with only the largest, most expensive, most dense urban centers impacted. It is a reversal that could change population and demographic trends for generations to come. Interest Rates What happens when interest rates are not set by market forces, but rather managed by policy? Jerome Powell, chair of the Federal Reserve, and Janet Yellen, immediate past chair of the Federal Reserve and current Secretary of the Treasury, have stated that they do not want to see interest rates rise. An increase in interest rates would make government borrowing more expensive. What are the impacts of a managed low interest rate environment? First, is the intended boost to consumption and investment. Because interest rates are low consumers and investors are incentivized to spend more. Housing is a good example. A 1% decrease in interest rates on a $350,000 home will allow the price to rise approximately 14% while the mortgage payment remains the same. In other words, the payment on a $350,000 house at 4% is approximately the same as the payment on a $400,000 house at 3%.  There is downside. First, if you are looking to earn a return on savings, you will be disappointed. This incentivizes savers to take additional risk and compete for other investments like stocks, bonds, and real estate—driving those assets values up. Second, the distortion makes government borrowing for federal, state, and local governments appear lower than it should be, incentivizing borrowing by government.

When interest rates become more about policy decisions than economics, unexpected distortions occur that are not healthy in the long run. Policy Distortions More than ever, economics is valuable in helping understand the result of policy choices. It is important to listen to what policy makers say, but it is even more important to watch what they do. Policy makers have often said they want to help individuals who have been hurt by the COVID-19 induced recession. More than once, they have issued checks of $1,400 to qualifying individuals. They have provided rental assistance and eviction restrictions. At the same time, interest rate policy has increased home values on average by $50,000 in the United States. This disparate impact has benefited homeowners and widened the wealth gap relative to those who rent. Policy makers have said the want to put money in families’ pockets to help them weather the pandemic. The combined relief packages of over $5.2 trillion in COVID-19 stimulus in the United States distributed to over 130 million households would have been $40,000 per household if distributed directly. If relief focused only on those who lost jobs during 2020, the combined relief packages for approximately 25 million lost jobs is $208,000 per lost job. Policy makers are concerned about large urban cities and their recovery. Structural shifts accelerating work from home options have released many from living in urban areas, and they have responded by moving to less crowded areas. The result is less traffic, less crime, better air, and better balance for relocating employees. The downside is less revenue to support urban infrastructure and programs. Policy makers have said they are concerned about getting Americans back to work. Many will stay out of the work force by no choice of their own until economies are open and policy makers trust citizens to make good decisions. Policy makers are concerned about equal opportunity for all Americans. There is no greater equalizer than education, yet in many communities our schools remain closed and those students who are least prepared to catch up are being impacted the most. Conclusion Unfortunately, as with most recessions, individuals are impacted differently. This recession is unique in that winners and losers are primarily determined by policy, not by economics. The response has been to stimulate the economy by lowering interest rates and fiscal spending of $5.2 trillion. Homeowners, suburban and rural communities, and essential services are winners that are benefiting from the upside in a “K” shaped recovery. Urban centers, renters, children, and low wage earners are feeling the downside. The policies of the last year are highly inflationary, even if inflation doesn’t show up in traditional consumption items such as food, fuel, or other household purchases. Asset prices are rising and will do so until the policy induced stimulus runs out.  Reduce Your Tax Liability, Buy Commercial Real Estate

If you have had strong income or expect to have a significant taxable income this year, investing in real estate may help. You can either pay the IRS, or do something they have incentivized you to do that allows you to keep your hard earned income. It is not unusual for the tax code to use taxes to incentivize certain types of investment. For example, if you make financial contributions to a qualified retirement accounts, those contributions are deductible and reduce your overall taxable income, which reduces the amount of taxes owed in the year you make the investment. Depreciation Benefits for Real Estate Real estate assets differ from financial assets like stocks in that a portion of real estate gets consumed with time and is replaced. A real estate asset is part indestructible asset (the land) and part consumed asset (the improvements). Tax law recognizes improvements are consumed by allowing investors to depreciate the improvements but not the land. Depreciation is the reduction in value over time for the normal wear and tear of an asset. The amount of depreciation allowed is determined by a schedule provided by the IRS. It has been known for many years that the IRS will allow a cost segregation study on real estate assets. This study is prepared by a professional who evaluates the real estate based on the property type, age, and nature of the improvements. Instead of being depreciated over 39.5 years, a cost segregation study separates the property into 5 year, 15 year, and 39.5 year improvements. For example, 15 year improvements are those improvements that have to be replaced in approximately 15 years because their useful life has been exceeded. This may include tenant improvements, the roof, or the HVAC system. Segregating improvements into their respective 5, 15, and 39.5 year useful lives provides larger deductions in earlier years relative to a standard 39.5 year depreciation schedule. Given that depreciation reduces taxable income and assuming that depreciation today is more valuable than depreciation in the future, accelerated depreciation is valuable. 2017 Tax Law Allows for Accelerated Depreciation President Trump’s tax law, Tax Cuts and Jobs Act, passed in 2017 made a substantial change to depreciation that benefits commercial real estate owners. It allows for 5 and 15 year property designated in a cost segregation study to be fully depreciated in the year the property is put in service. That means that if you purchase and put in use a property in 2020 and the property has $500,000 in 5 and 15 year improvements, then the owner could deduct up to $500,000 in depreciation in 2020. Also significantly, the tax law in certain cases authorizes you to use the depreciation benefits to offset prior year income. You need to discuss this with your tax professional to determine if you qualify for this treatment. Exhibit 1 shows a hypothetical $1,750,000 investment purchase where the value is allocated to land ($437,500), 39.5 year improvements ($812,500), and 5-15 year property ($500,000). In year 1, without cost segregation and accelerated depreciation, the straight line benefit on the 5 and 15 year property is $50,000 * 35% (the hypothetical tax rate), or $17,500. Under the 2017 tax law, additional depreciation benefits in Year 1 are $450,000, which at a 35% tax rate are worth $157,500. This means that in the year this hypothetical property is put into use, buying the property could save the investor $157,500 in income tax expense—or 9% of the property value. There is always a catch. Accelerating depreciation reduces your basis in the property so that when it is time to sell, your gain is larger than if you had not accelerated the depreciation. That means your tax liability is larger when you sell in the future. Of course, you can exchange the property and defer the tax liability even further by utilizing a 1031 exchange. What About Investors? The best benefits are for property owners, but investors can accelerate depreciation to offset up to 100% of the future income generated from the project. As always, please consult your tax professional to determine how the new tax law applies to you. Conclusion There are may investment opportunities available to investors. All of them have their respective benefits. Financial assets like stocks, bonds, and mutual funds can be held in tax deferred accounts that allow for investments to accumulate while deferring tax liability. Benefits to owning real estate include the ability to depreciate the consumable portion of the asset over its useful life. The depreciation benefits are set by the IRS and were revised in the 2017 Tax Cuts and Jobs Act. The revision resulted in the ability to accelerate depreciation and reduce taxable income today. This can be a valuable benefit for investors looking to offset taxable income from real estate investments.   The United States government struggled with the COVID-19 recovery bill to address the recession the government created. It will not be implemented but here is my proposal (skip to #5 below if you are in a hurry).

1) The bill that is being considered is enormous and highly inefficient. It will get passed anyway. 2) We should not subsidize state and local governments. They made the decision to go into recession, their revenues are protected (utilities, property taxes, income taxes). Sales tax has exposure, but it has always been more volatile than income and property taxes. 3) We should not subsidize businesses or industries. Their assets will be bought and the human capital will not be destroyed. Let the situation play out with investors and creditors. 4) We should not try and solve the situation through unemployment insurance. It is too bureaucratic. The money will not get distributed when it is needed, and then too much will get distributed when it is not needed. 5) There are approximately 130 million households in the United States. Congress will approve an astounding $2 trillion dollar package. That is $15,000 per household. Why not send every household $15,000? The IRS can claw back unneeded funds on next year’s tax return for those who do not lose their job and who make over $100,000 per year. If someone loses their job or does not make over $100,000 per year, then let them keep the money. We are a consumption based economy. The business sector will weather the recession if consumers are not scared and broke. The payments will allow everyone to either get through the next couple of months or have some reserves set aside. Those who don’t end up needing it can return it on the next tax return. The rest of the country will be set to deal with the recession the government created. This solution can be executed fast, it is easy to implement, and easy to administer.

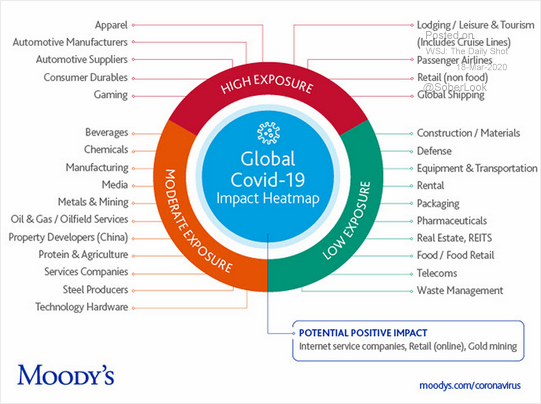

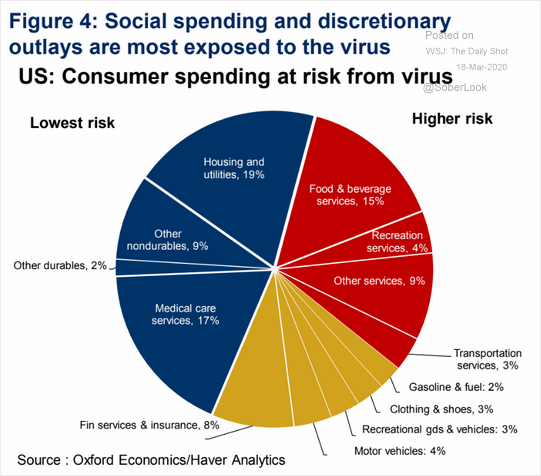

We are in Recession The United States moved into recession because of COVID-19 and subsequent governmental actions. It hasn't been confirmed by official statistics, that will take time. A recession is defined as two consecutive quarters of falling Gross Domestic Product (GDP). The first quarter of 2020 will show a small drop in GDP because of COVID-19 personal distancing measures and impacts to nonessential business implemented by governments in March. The second quarter will be a much larger drop due to the impacts. Which Sectors Will Be Hurt the Worst? High exposure sectors include hospitality, travel, tourism, restaurants, airlines, and other businesses that put groups of people in close contact. The personal distancing measures governments have implemented will create residual reluctance for people to be in large groups and will slow recovery for some businesses. Further, any business or activities considered nonessential will be slower to rebound. Who are the Winners? First, winning in a recession is relative. Some will see revenues rise, but some may simply see revenues not fall as much as harder hit sectors. Delivery services will do well, online merchants will benefit. Personal services offered in homes will benefit. Healthcare, domestic manufacturing, transportation, housing, internet and communications services, and utilities considered essential will be more resilient and some will see upside. Not the Same as Last Time Each recession and recovery is different. The last recession was characterized by a surplus of homes built by home builders and inflated buyer demand from real estate investors buying homes no one planned to live in. It was made possible by the underwriting of loans where borrowers didn't have sufficient income to support the debt service. Contrast this with current real estate markets. First, home builders have built many homes, but in some cases at half the rate of the last market cycle. There is very little standing inventory, and the homes have been purchased by people who will occupy them, or investors with someone to rent them. Further, when the loans were originated, the investors who purchased the homes had the income to support the investments. This recession was initiated by COVID-19 being declared a global pandemic and the actions of governments to implement personal distancing and close nonessential businesses. The government knowingly put the United States in recession in an effort to stop a global pandemic. There will be softness in real estate. New home construction will be impacted more than residential resale. Expensive markets will be impacted more than affordable markets. Low growth markets will be impacted more than high growth markets. Retail will be impacted more than industrial. Hospitality and vacation rentals have the most exposure today. Interest rates will be low and there will be opportunities for buyers. Recovery The economy will adapt and recover. This recovery will be much quicker than the last one, but it still will take time. Unemployment will rise quickly and the hiring will be slow to recover because of an abundance of caution from employers. Recovery will begin when collective economic activity stops falling and starts growing again. The start of the recovery is not intuitive. It is when everything seems to be the worst. We call this the trough. The recovery lasts until we reach the peak of the last market cycle, which will be the fourth quarter of 2019. From there, we will resume economic expansion. Looking Ahead Everyone will adapt. Some adjustments will be easy, some will be hard. Individuals and businesses will make adjustments and we will begin a recovery. Some basic principles will persist. First, have cash set aside for a rainy day. Second, you can't get credit when you need it most. Secure credit when times are good. Third, change is inevitable. We can't always predict the source of change, but we can adapt and be responsive to change. Our world changed in the matter of a few months. The more quickly we make adjustments, the quicker we will begin the process of recovering.  |

RSS Feed

RSS Feed